The Impact of Life Science Tools on Scientific Progress

From Antonie van Leeuwenhoek using his microscope to make the first observations of bacteria through the sequencing of human DNA to recent work showing the potential to diagnose breast cancer from a fingerprint, tools have been the foundation of life science research. In my years of experience in this field, I’ve witnessed first-hand how these tools have revolutionized research and development. With emerging trends such as precision medicine and personalized healthcare, the importance of these tools is only set to increase.

In this blog series, I will explore the business and technology of the life science tools industry. My hope is to start a dialog about the promise and challenges in this important area.

The Life Science Tools Market

The life science tools market is attractive and bustling with innovation and growth. It’s a sector marked by high profitability, stringent regulations, and rapid technological advancements. Companies like those highlighted below are solving problems in life science research with their cutting-edge products.

The market includes both the broad pharmaceutical and in-vitro diagnostics segments. These segments are attractive for tools providers for several reasons:

- They exhibit consistent growth.

- They are profitable.

- They are regulated (more on this later).

- They address high-value problems driven by needs in healthcare.

- Products sold into these segments, if differentiated, enjoy very long product life cycles.

- There are opportunities to generate profitable and predictable revenue annuities in services, consumables, and software.

Regulations present both challenges and opportunities. They create entry barriers for newcomers, causing long selling cycles that put pressure on the returns of new entrants. The high switching costs for customers, due to both validation costs and the risk of issues, provide a significant advantage for incumbents. If the products are consistent and the service is good, customers have little incentive to switch. Analysts often refer to the “moat” of incumbency and the “stickiness” of products, including capital, consumables, software, and services.

Challenges and Opportunities in Healthcare

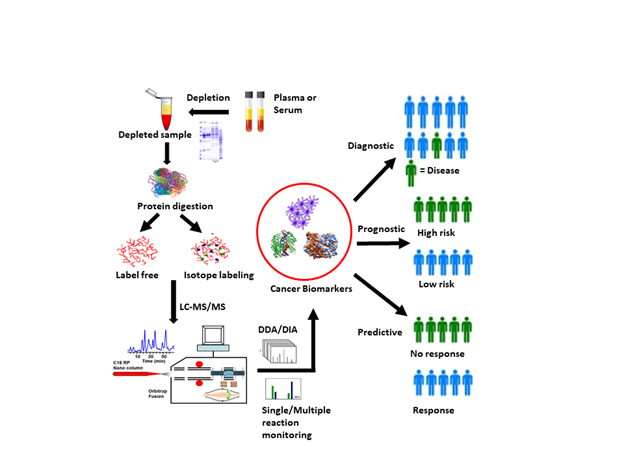

At the scientific frontier of medicine and diagnostics, there are high-value technical problems to be solved, and tools often play an enabling role. Today these problems include things like metabolomics and proteomics for the development of therapies and routine diagnostics. This drives innovation, with the winners reaping the benefits of long-term revenue annuities.

Risks also exist for participants in this market. Price controls pose a threat to the investment required to bring innovations to market for both pharma companies and tools providers. The advent of AI and cloud technology has the potential to disrupt the space. The push for data aggregation across healthcare could lead to the commoditization of tools, with value capture shifting to enterprise-scale software.

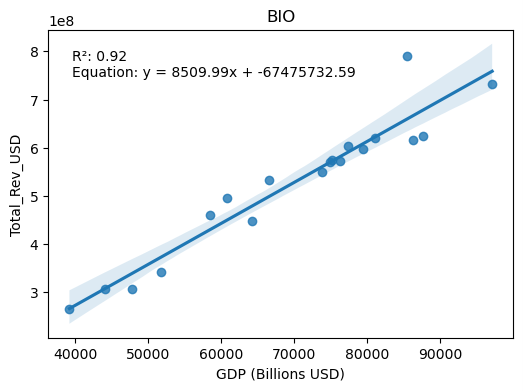

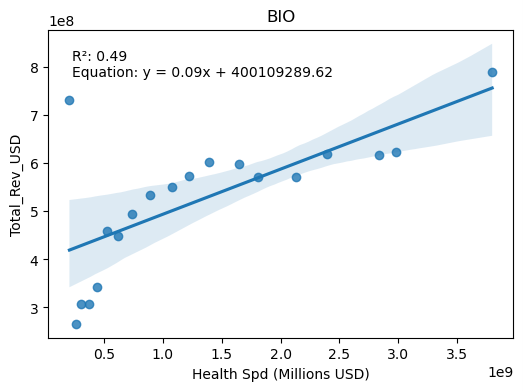

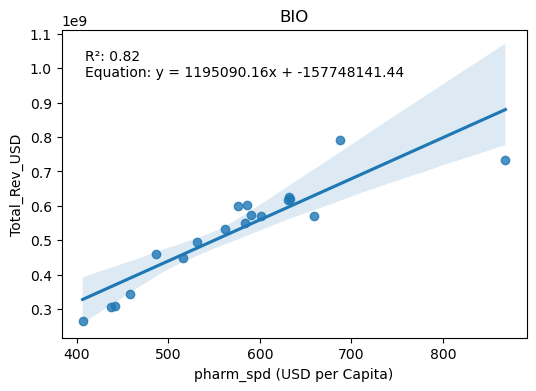

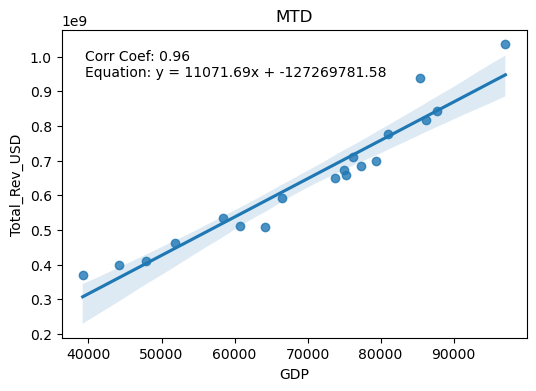

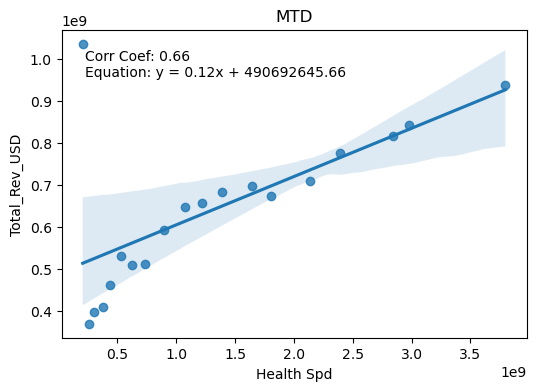

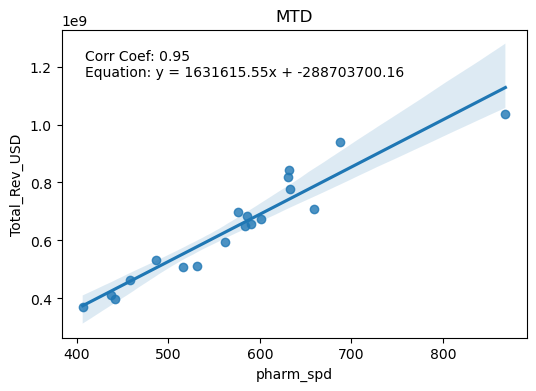

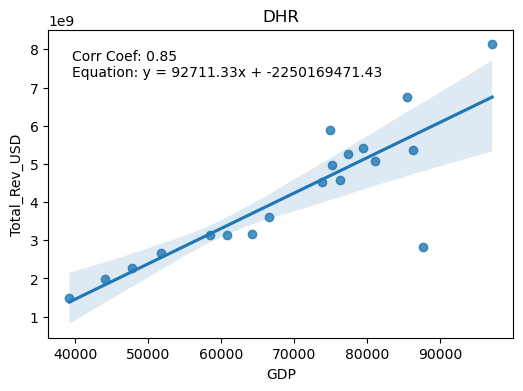

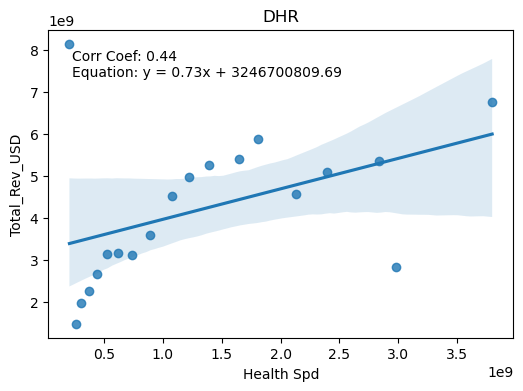

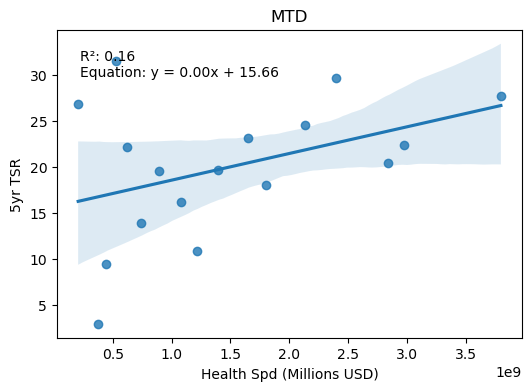

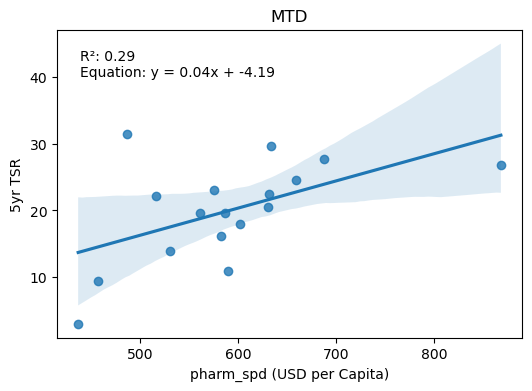

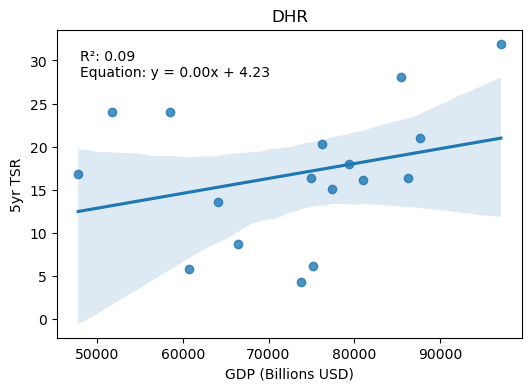

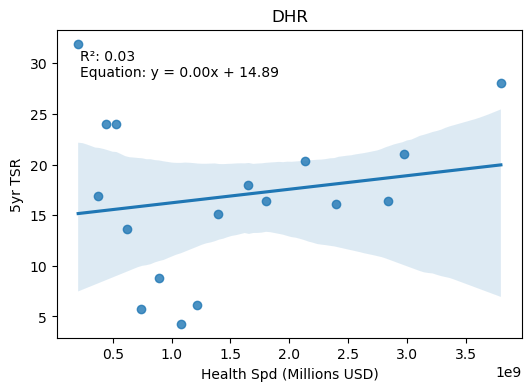

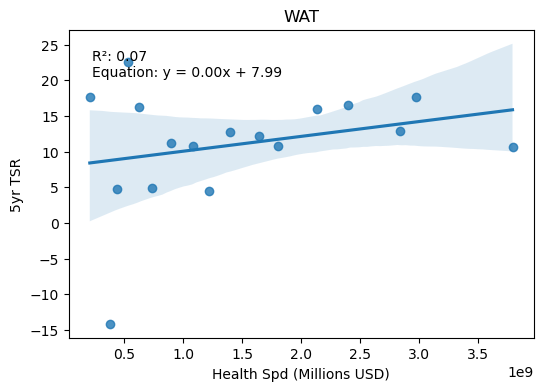

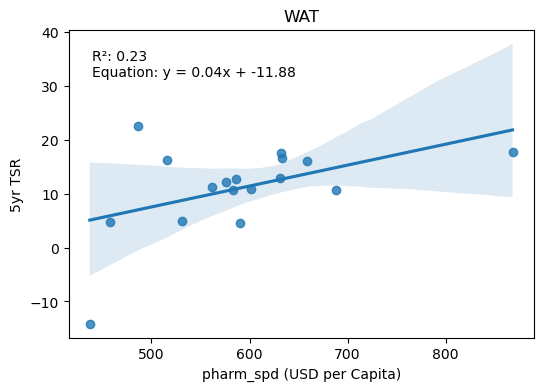

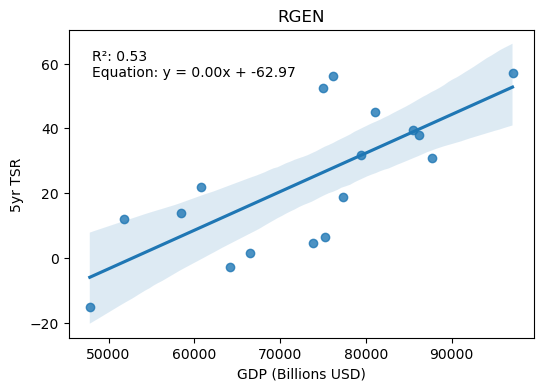

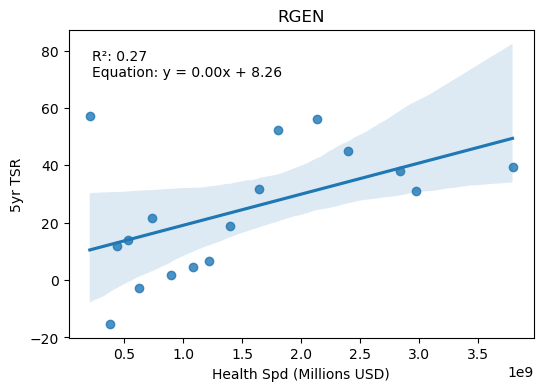

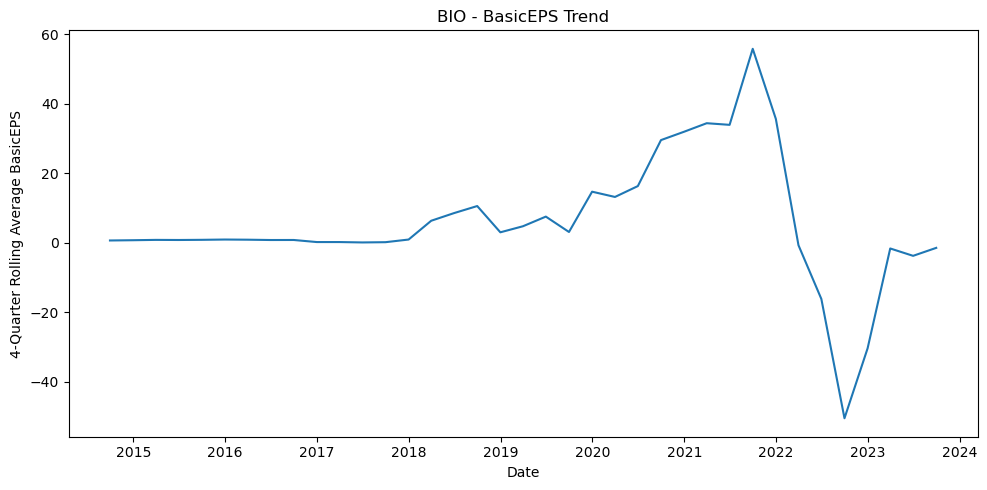

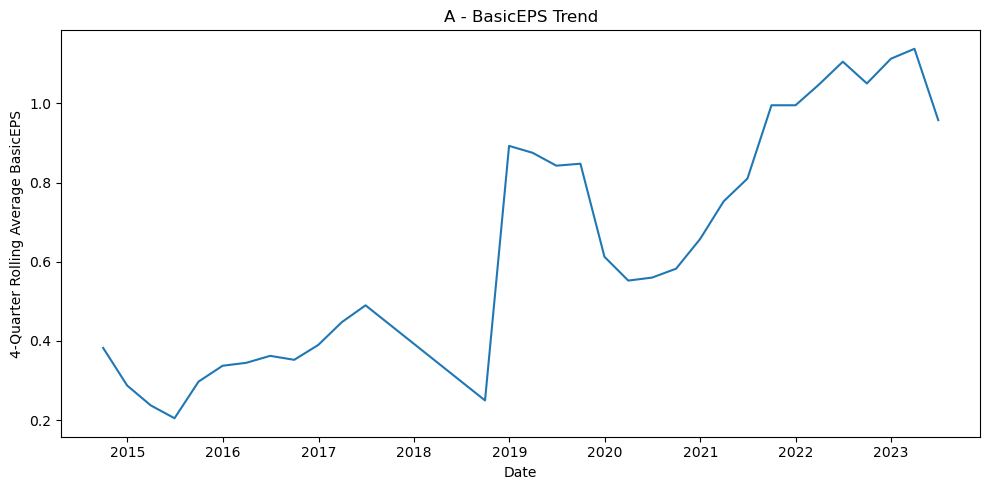

Financial Analysis

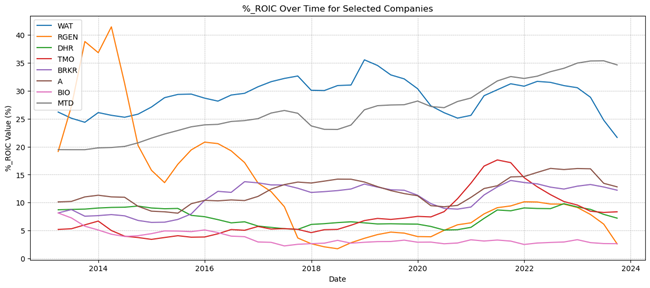

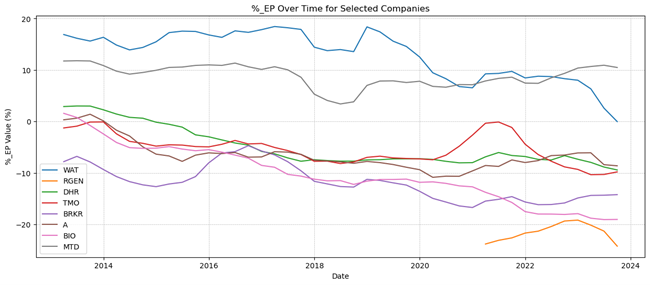

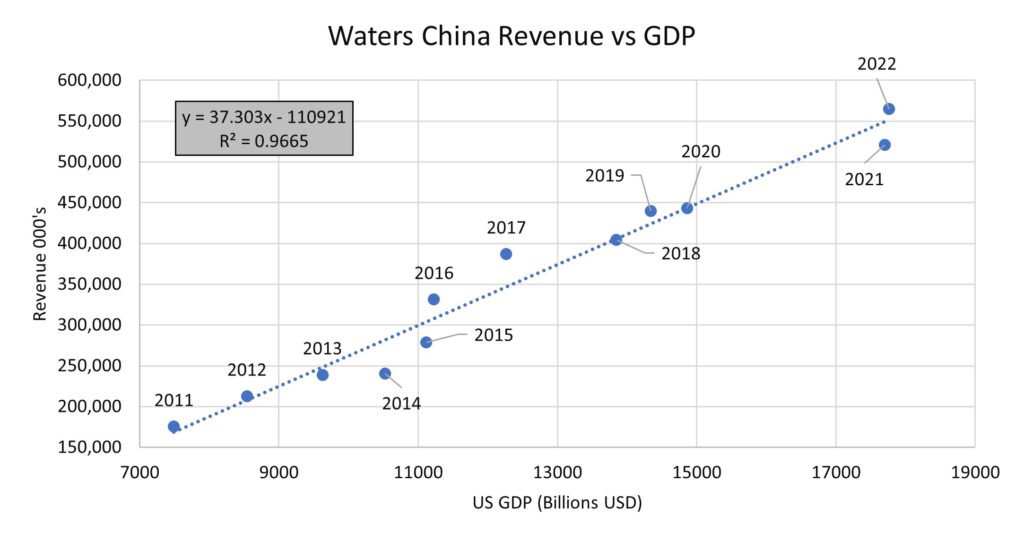

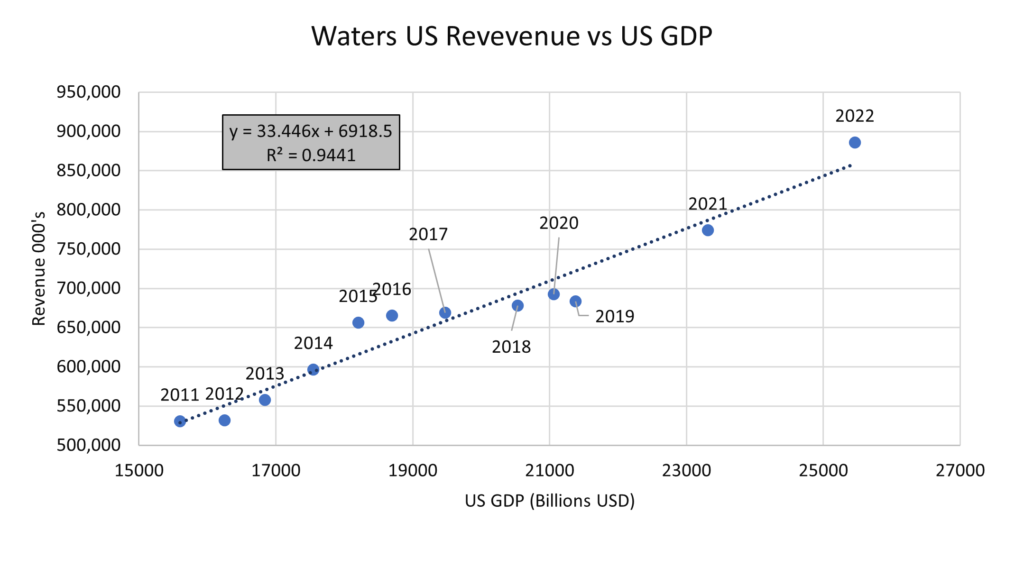

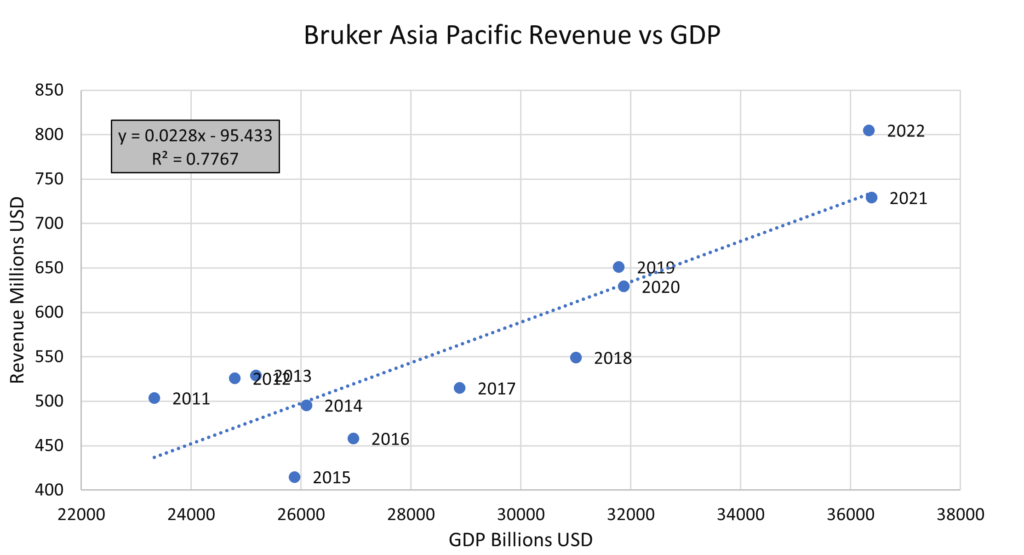

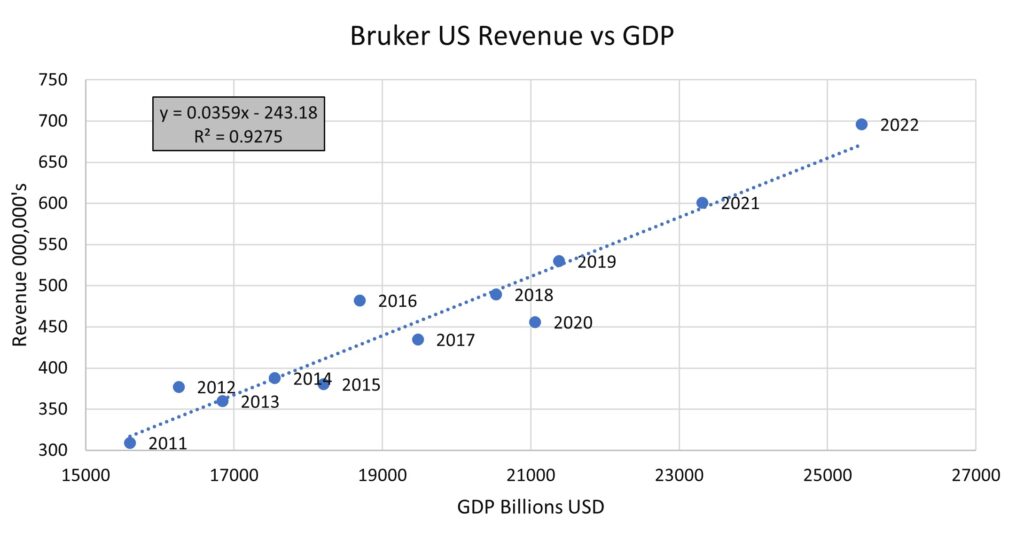

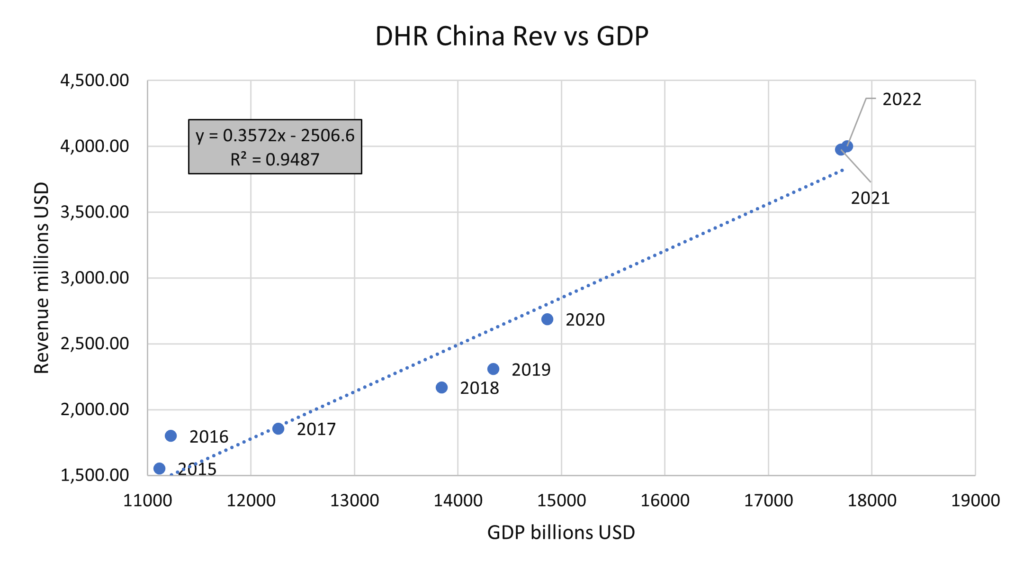

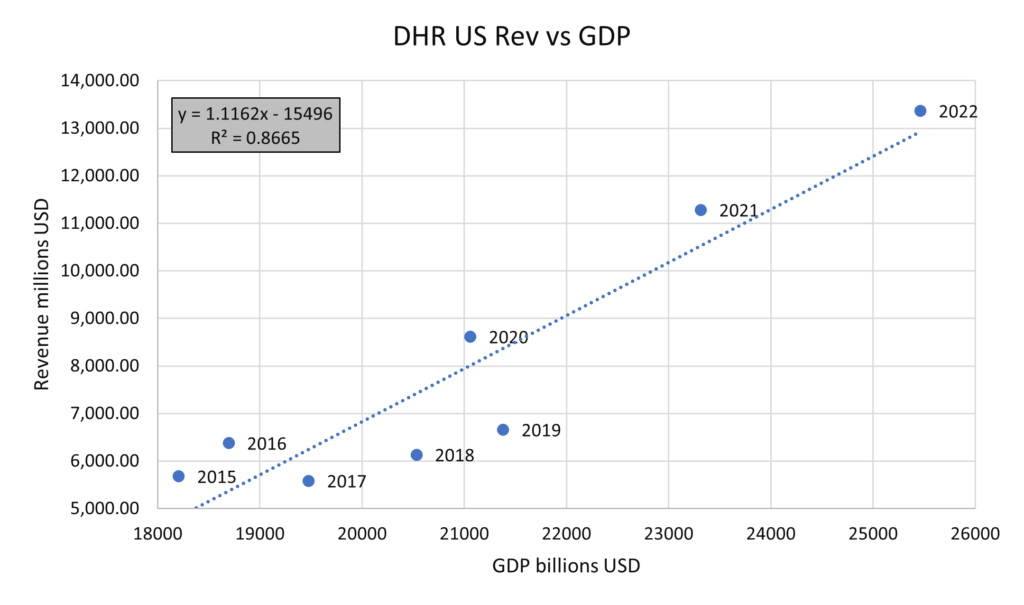

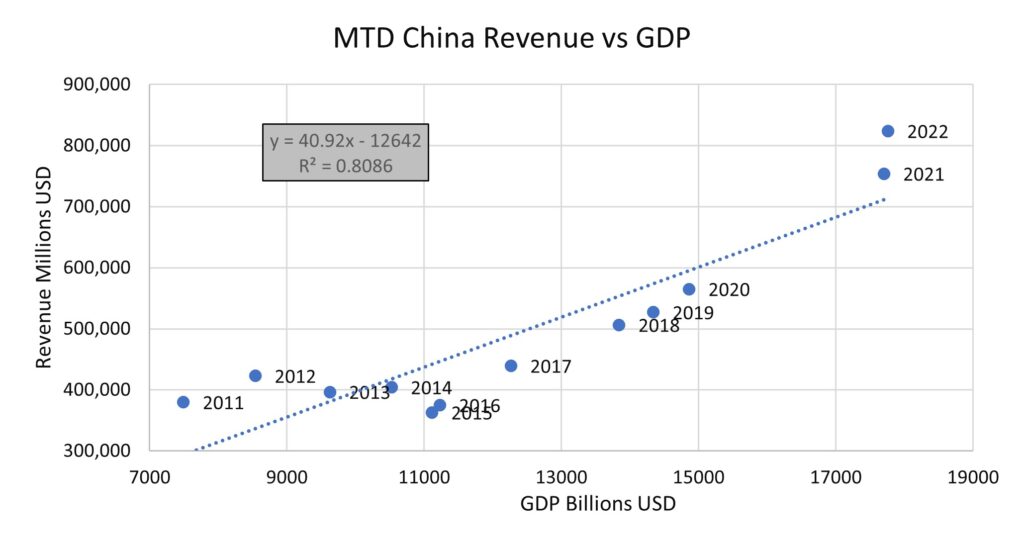

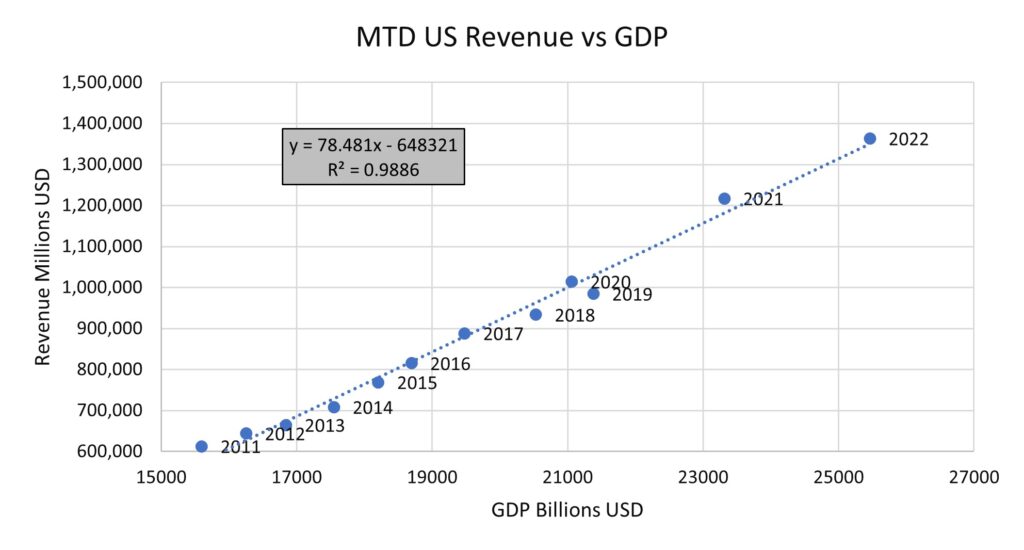

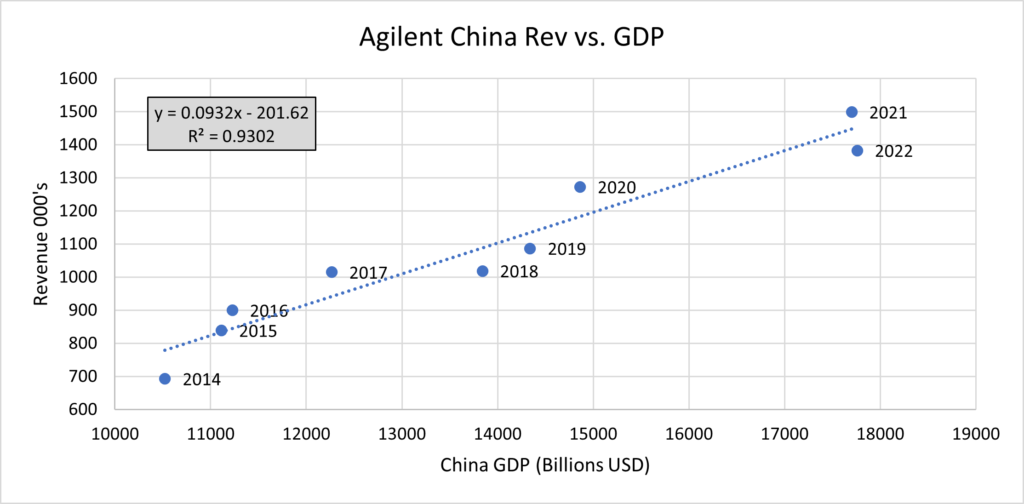

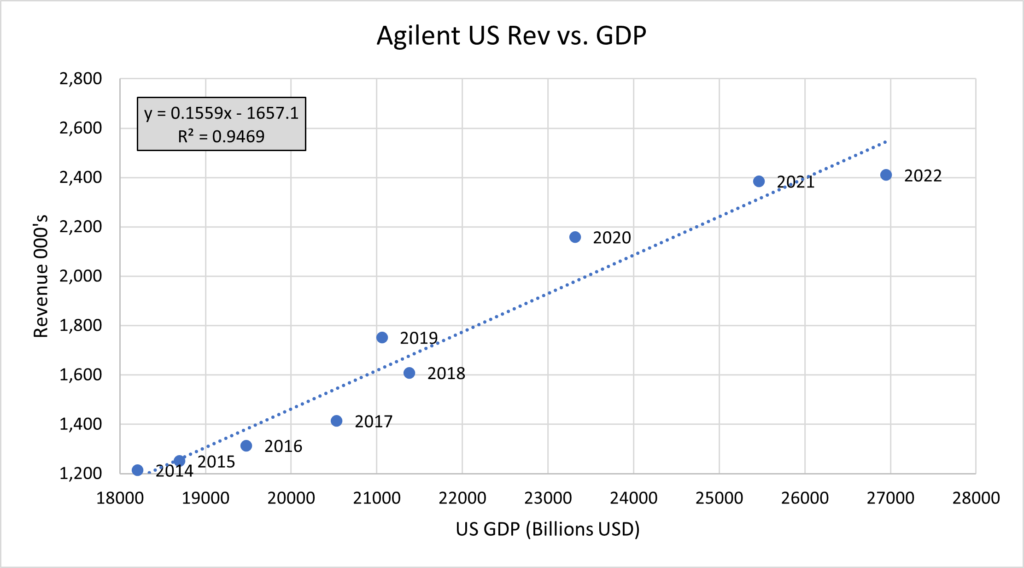

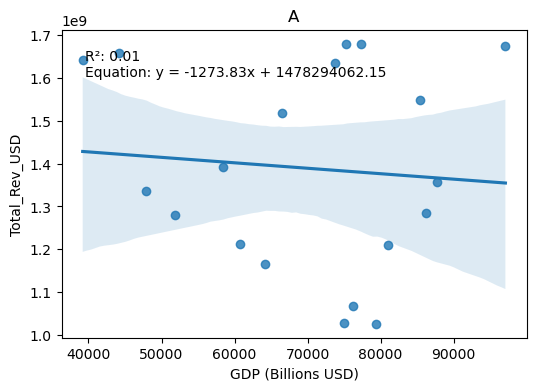

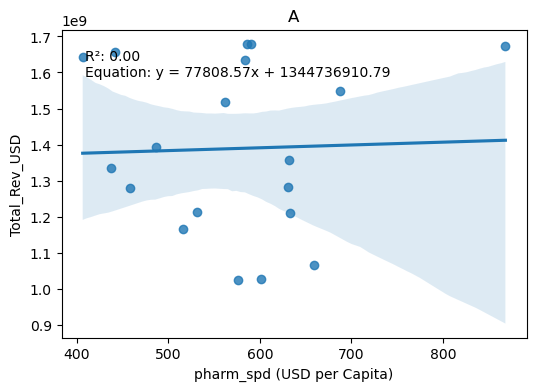

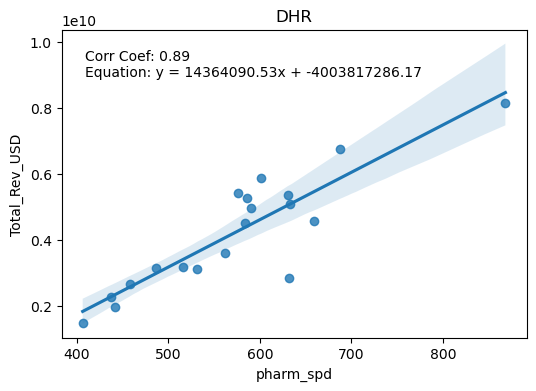

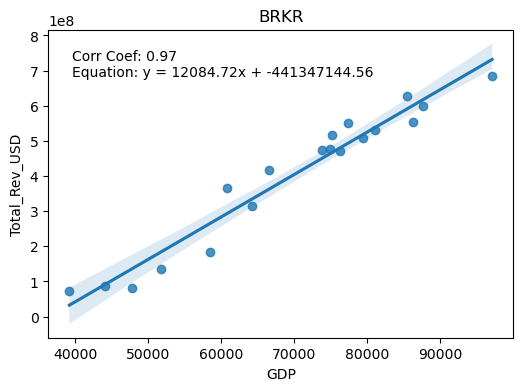

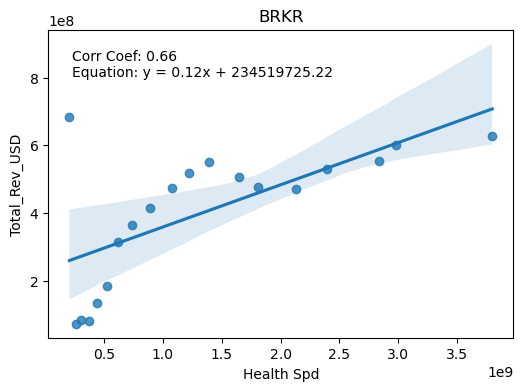

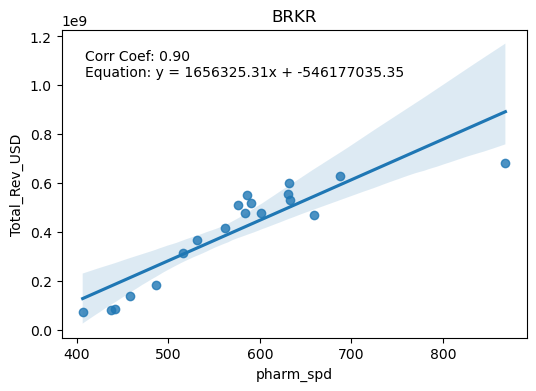

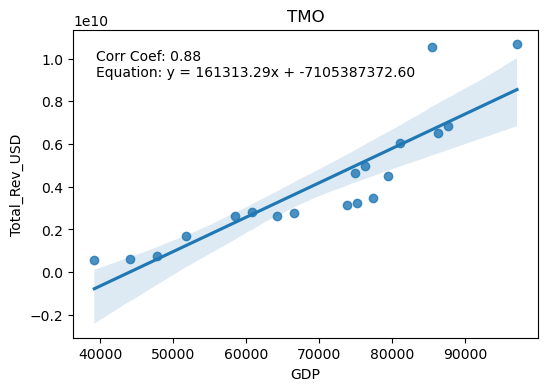

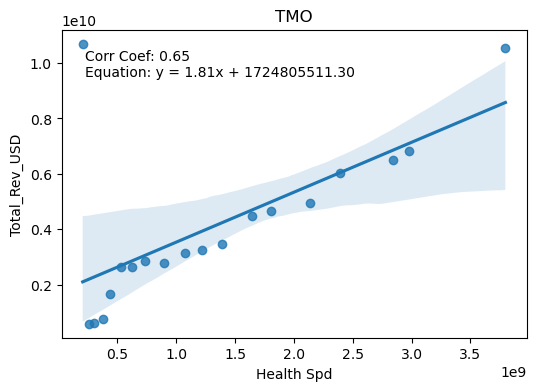

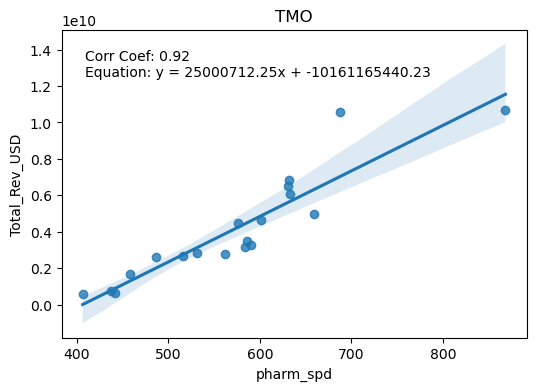

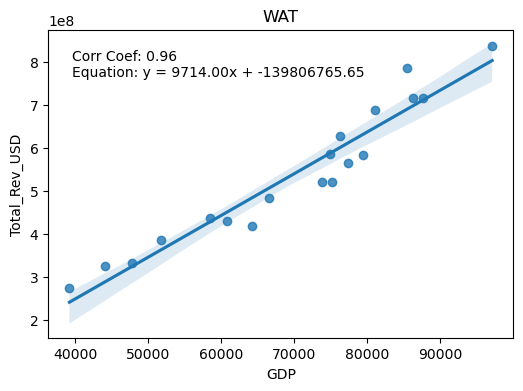

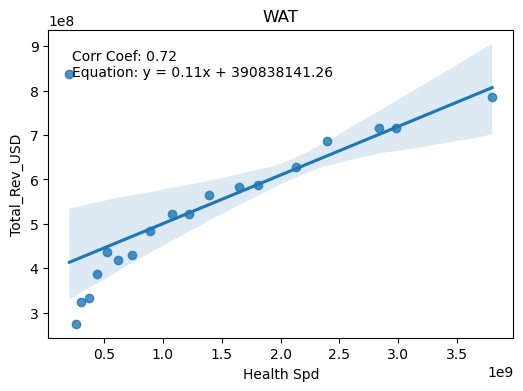

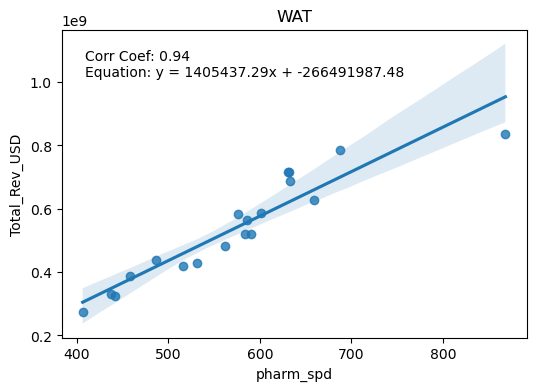

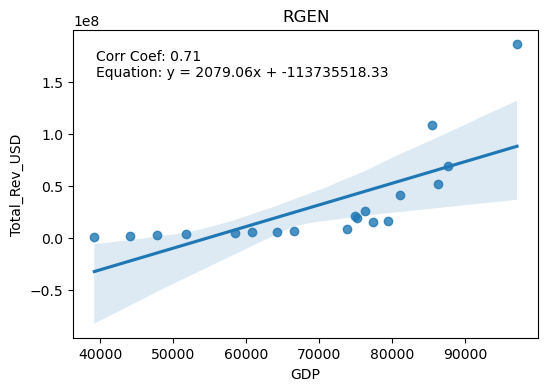

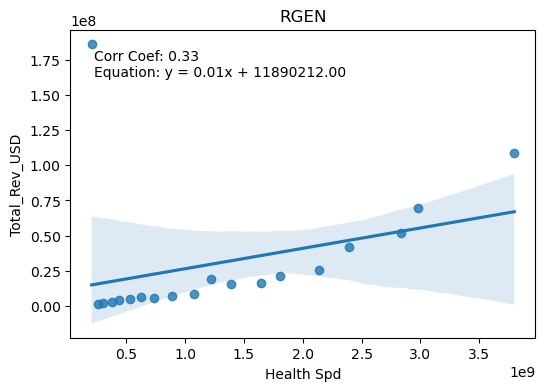

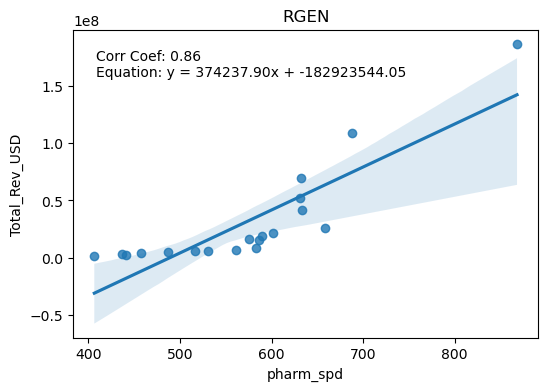

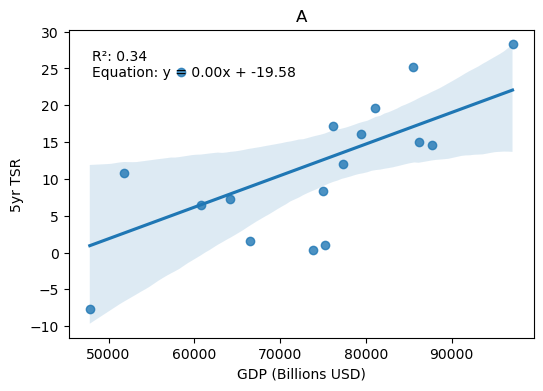

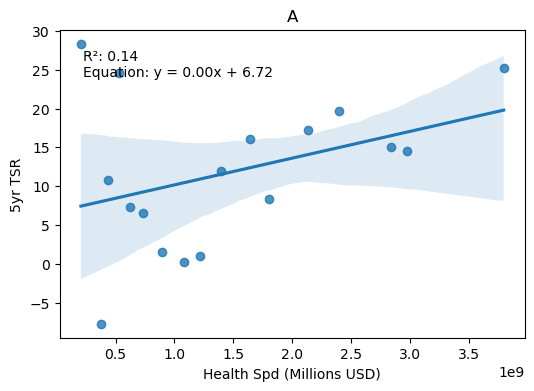

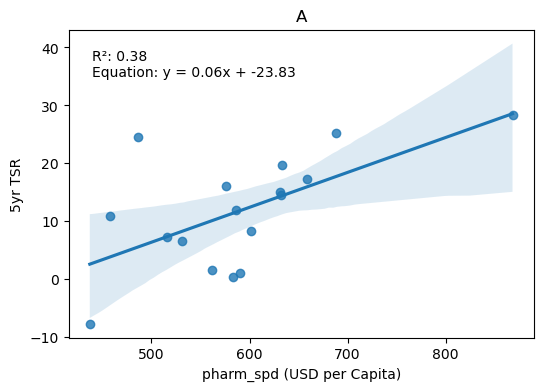

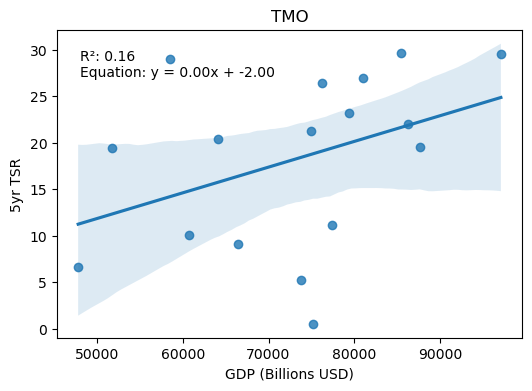

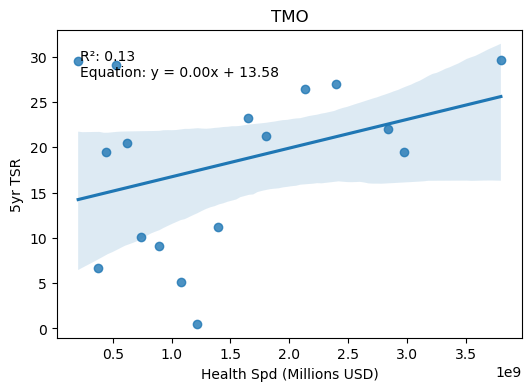

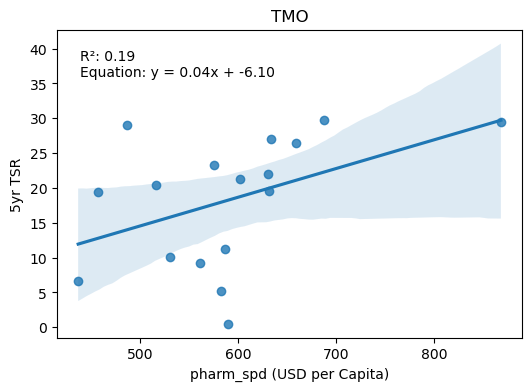

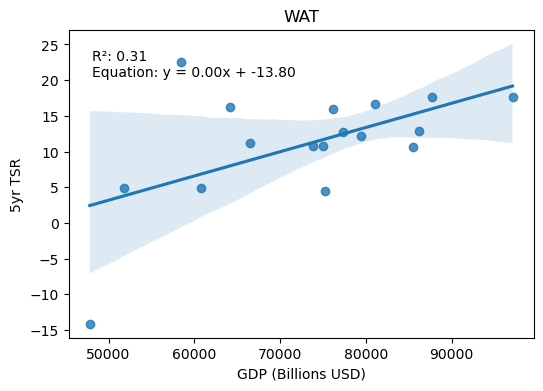

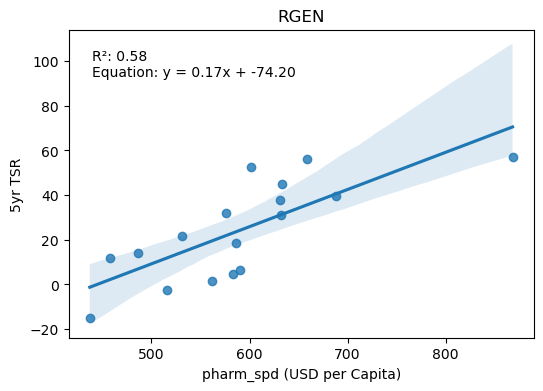

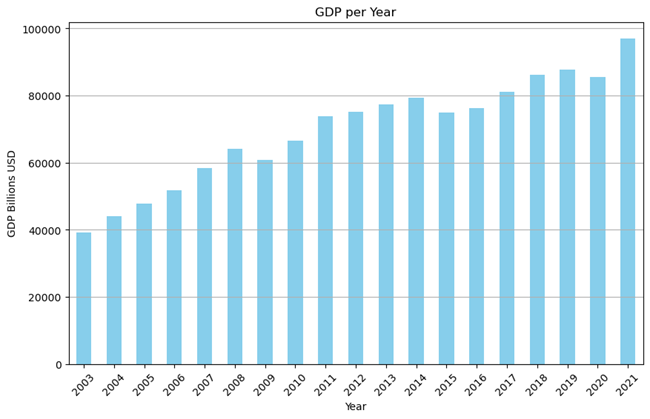

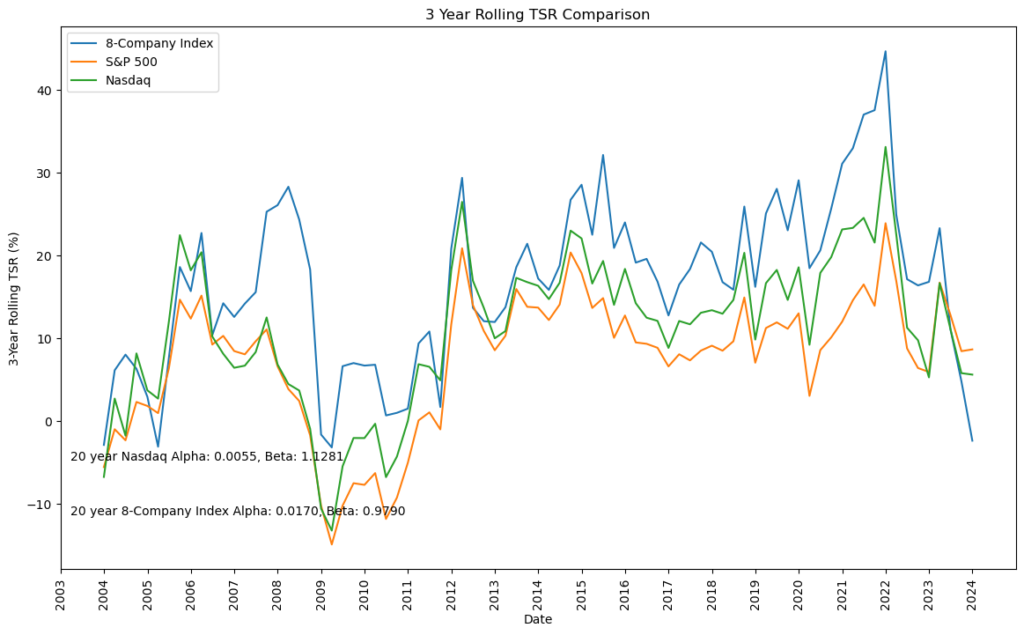

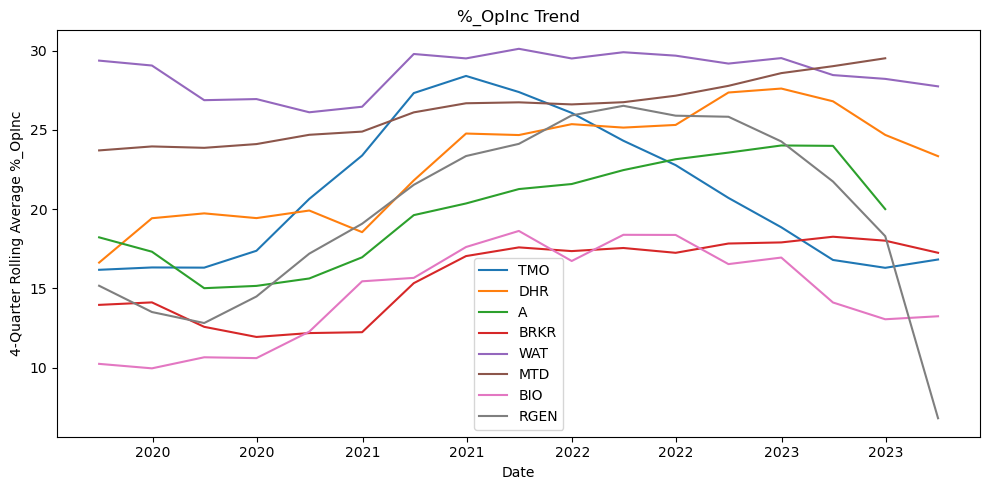

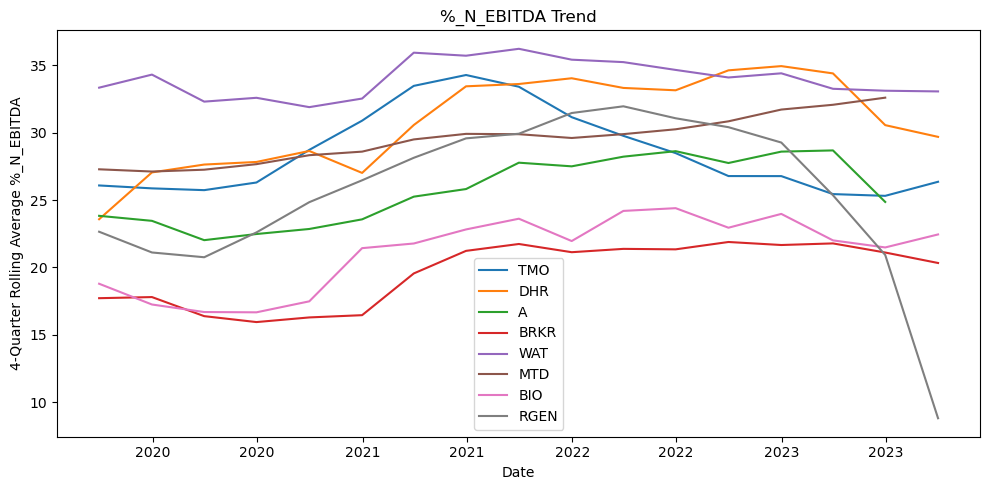

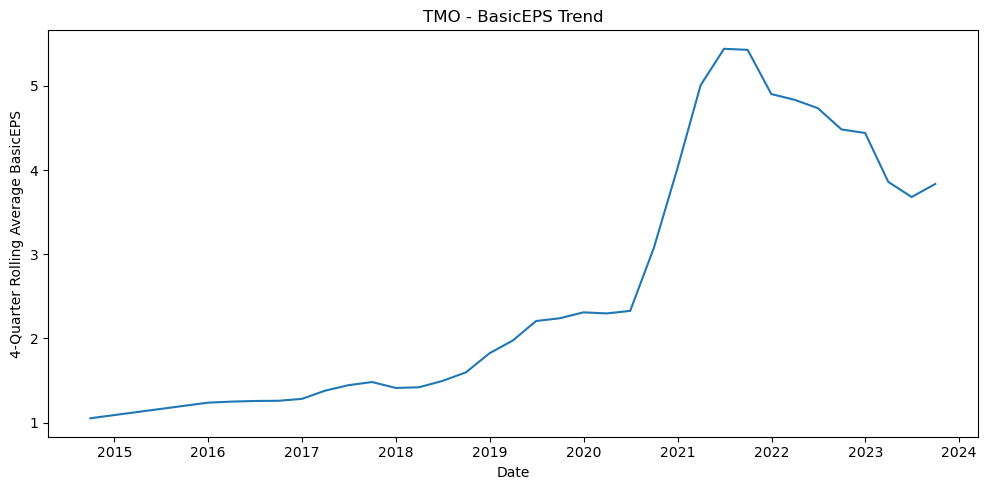

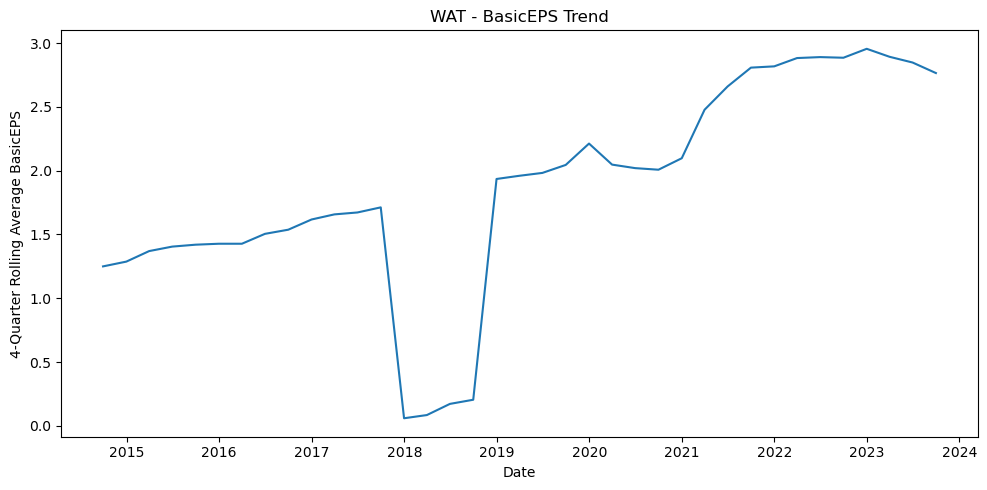

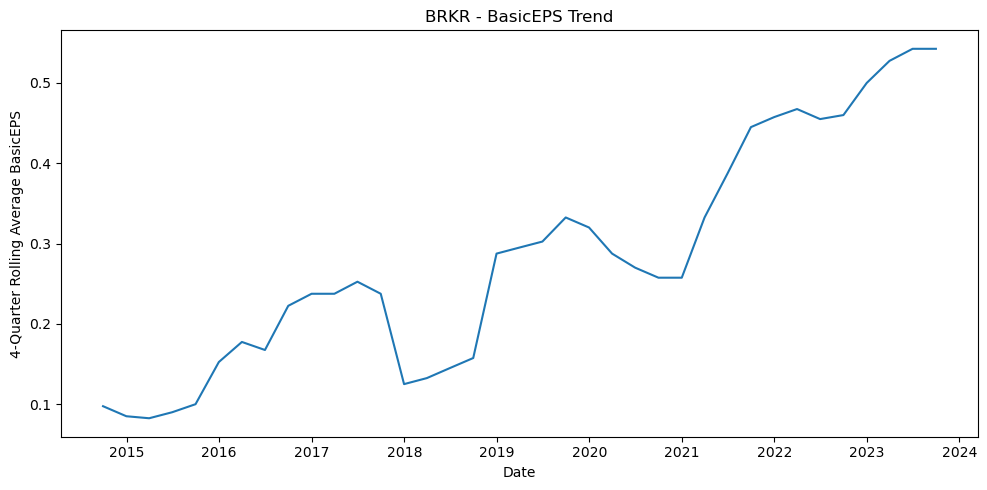

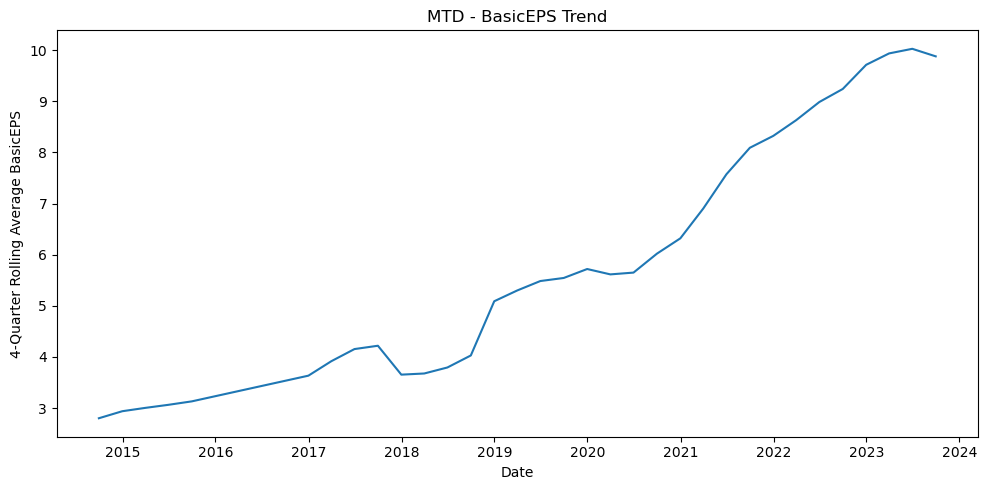

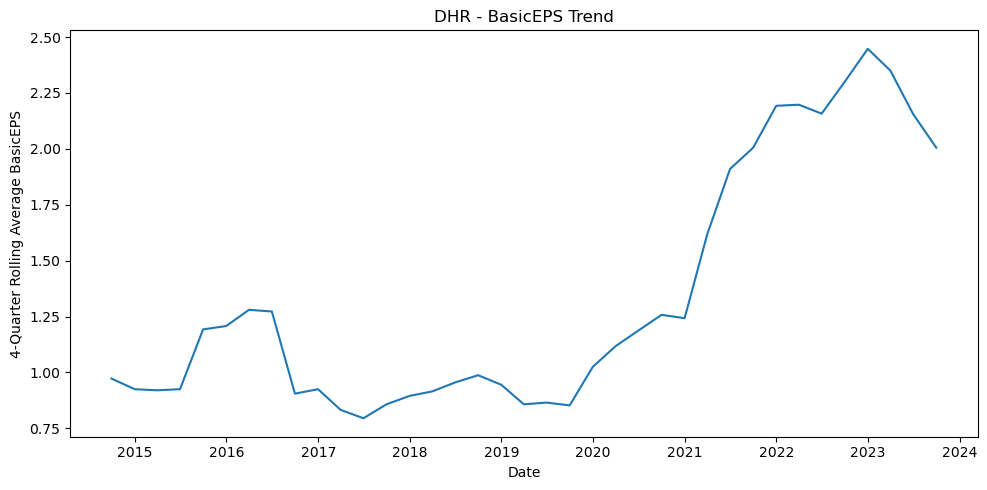

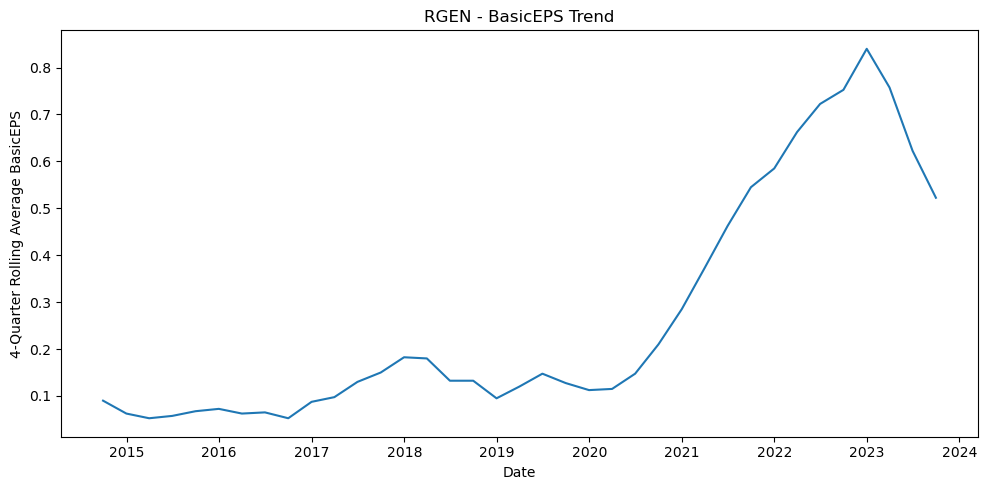

Understanding the drivers of shareholder returns in the life science tools industry requires a nuanced approach. I began by looking at a cohort of eight companies: Thermo, Danaher, BioRad, Mettler Toledo, Repligen, Bruker, Agilent, Waters. Using publicly available data from the companies, the SEC and Yahoo Finance I built a database compiling quarterly data from the P&L, Balance Sheet and Statement of Cash Flows. I then did some fundamental comparisons looking for simple correlations of shareholder return with macroeconomics and company financials. My analysis, which includes a machine learning evaluation of financial data, reveals some intriguing patterns. These insights are just the tip of the iceberg, and I plan to delve deeper in future posts.

In each BLOG I will dive into a different analysis. I will post a summary in the BLOG with more detail on my website –https://mthopeconsulting.com/life-science-tools-blog/. I’m open to feedback and suggestions for where to take this work.

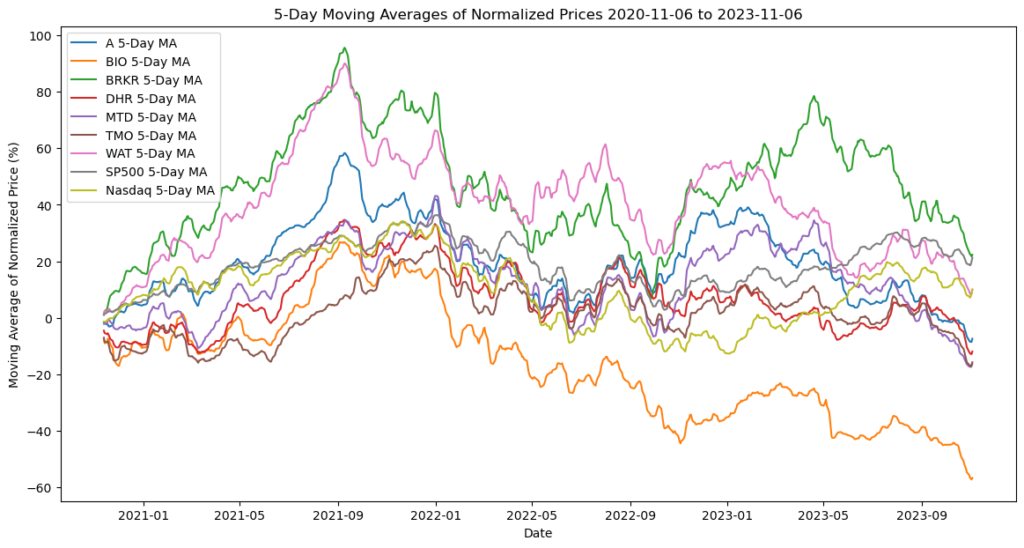

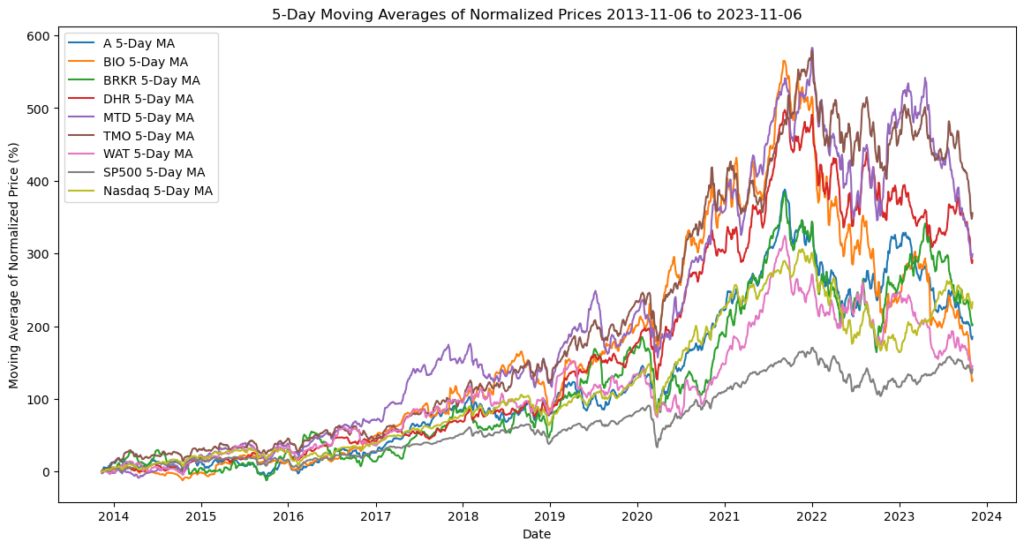

Stock Price Performance

To put things in context let’s first look at the stock prices of the eight companies over the past three years. I have used a moving average to filter the noise and normalized the companies and indices so I could compar